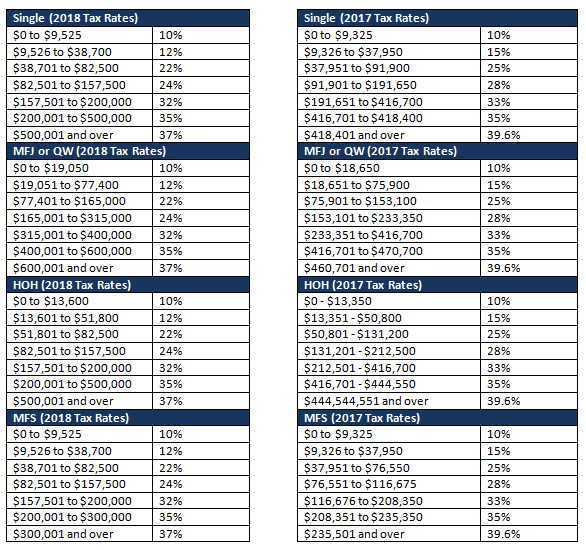

The following charts compare prior tax rates, brackets, phase outs and deductions with newly enacted legislation beginning in 2018.

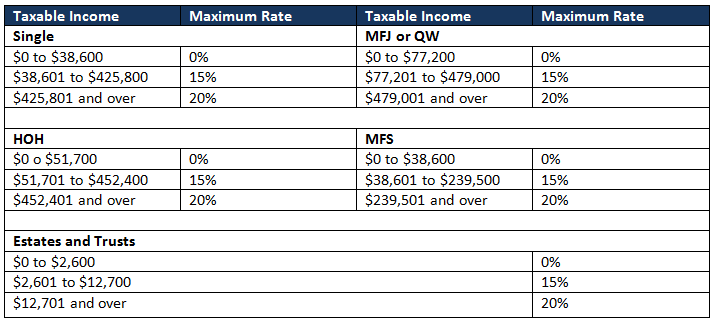

The Estate and Trusts Income Tax Rates have been revised as well. These changes are as follows:

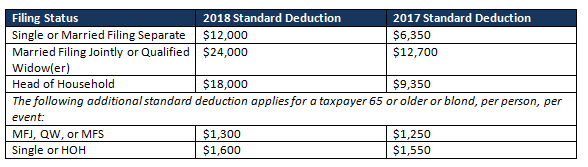

The Standard Deduction has been increased substantially. These changes are as follows:

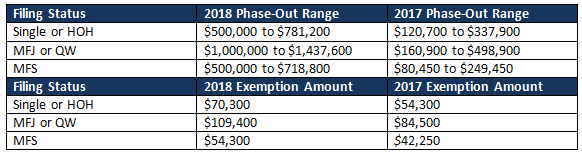

The 2018 alternative minimum tax (AMT) exemption and phase-out ranges have also been increased, greatly reducing the number of taxpayers affected by it. These changes are illustrated here:

The long-term capital gain and qualified dividend income maximum tax brackets no longer follow the tax brackets for regular income tax purposes.

The parent’s rate is no longer used to calculate the kiddie tax. Instead, taxable income attributable to net unearned income is taxed at the estates and trusts tax rates for both ordinary income and net capital gains.

The Tax Cuts and Jobs Act has opened the door for all new planning opportunities that when proactively administered, can save small business owners a substantial amount of personal income tax. The following is just a broad overview of some of the recent changes.